now loading...

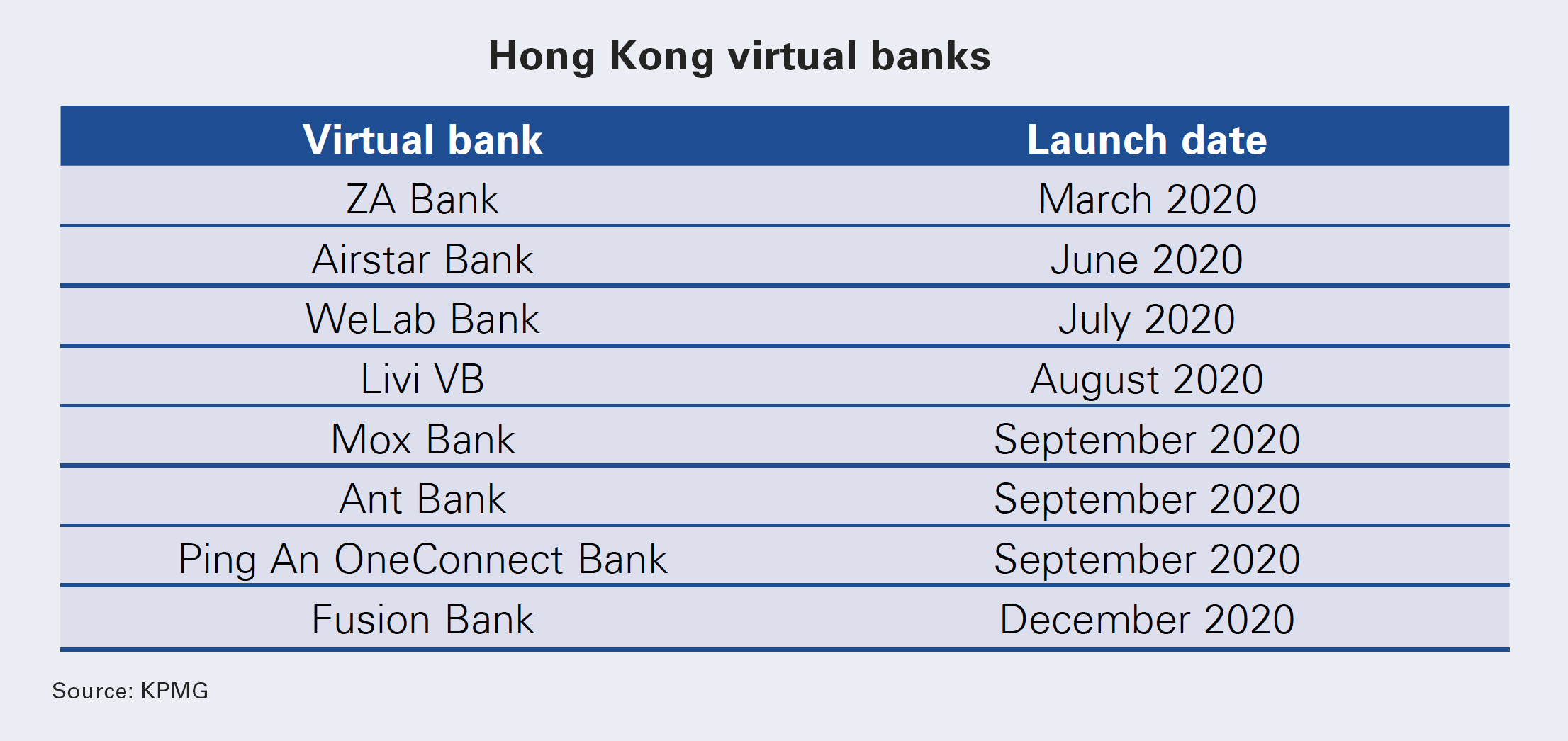

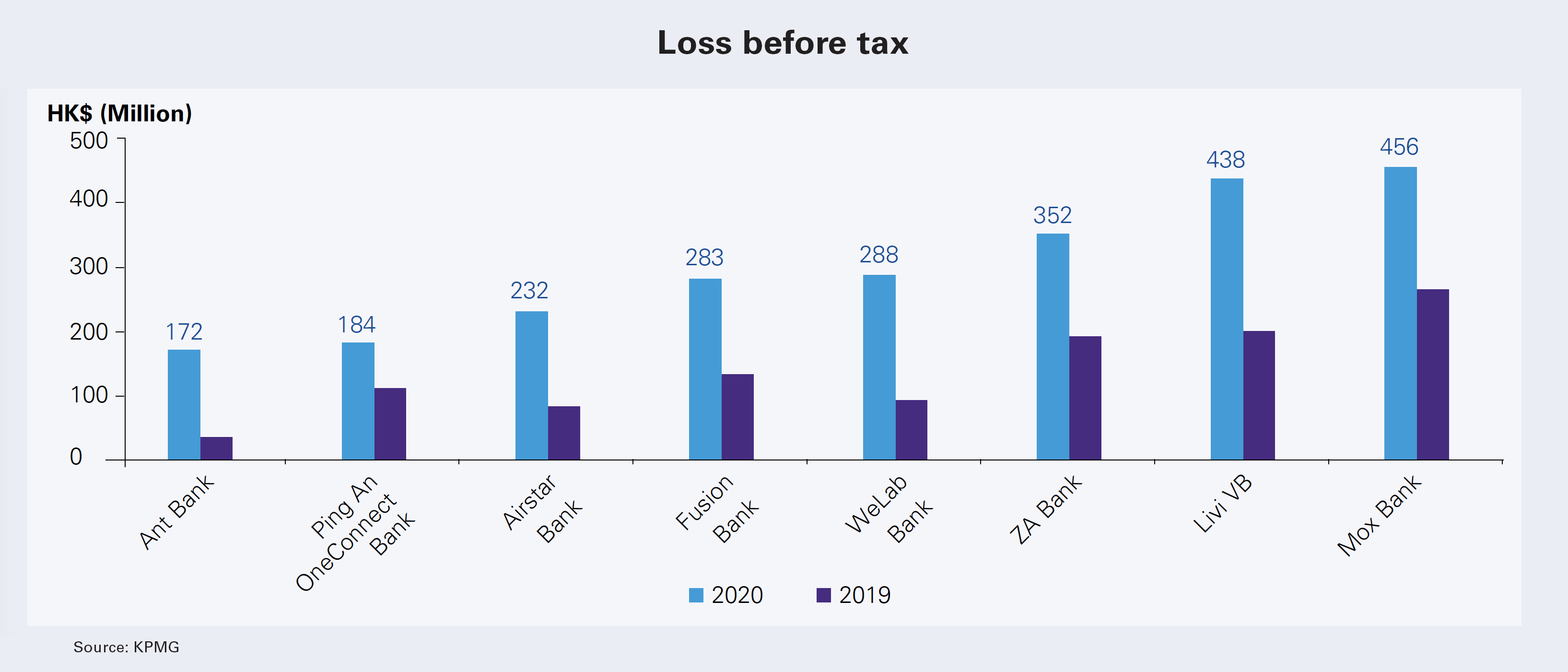

Hong Kong’s virtual banks need to continue evolving and expanding their offerings to make headway in a highly competitive environment. The city’s eight online-only lenders, which received their licences in 2019, have yet to turn a profit about a year after starting operations in the midst of the coronavirus pandemic.

This is understandable as they remain focused on investing and spending on areas such as office premises, staff costs, and information technology, as well as on marketing activities to grow their customer base, according to accounting major KPMG in its latest report on the Hong Kong banking industry.

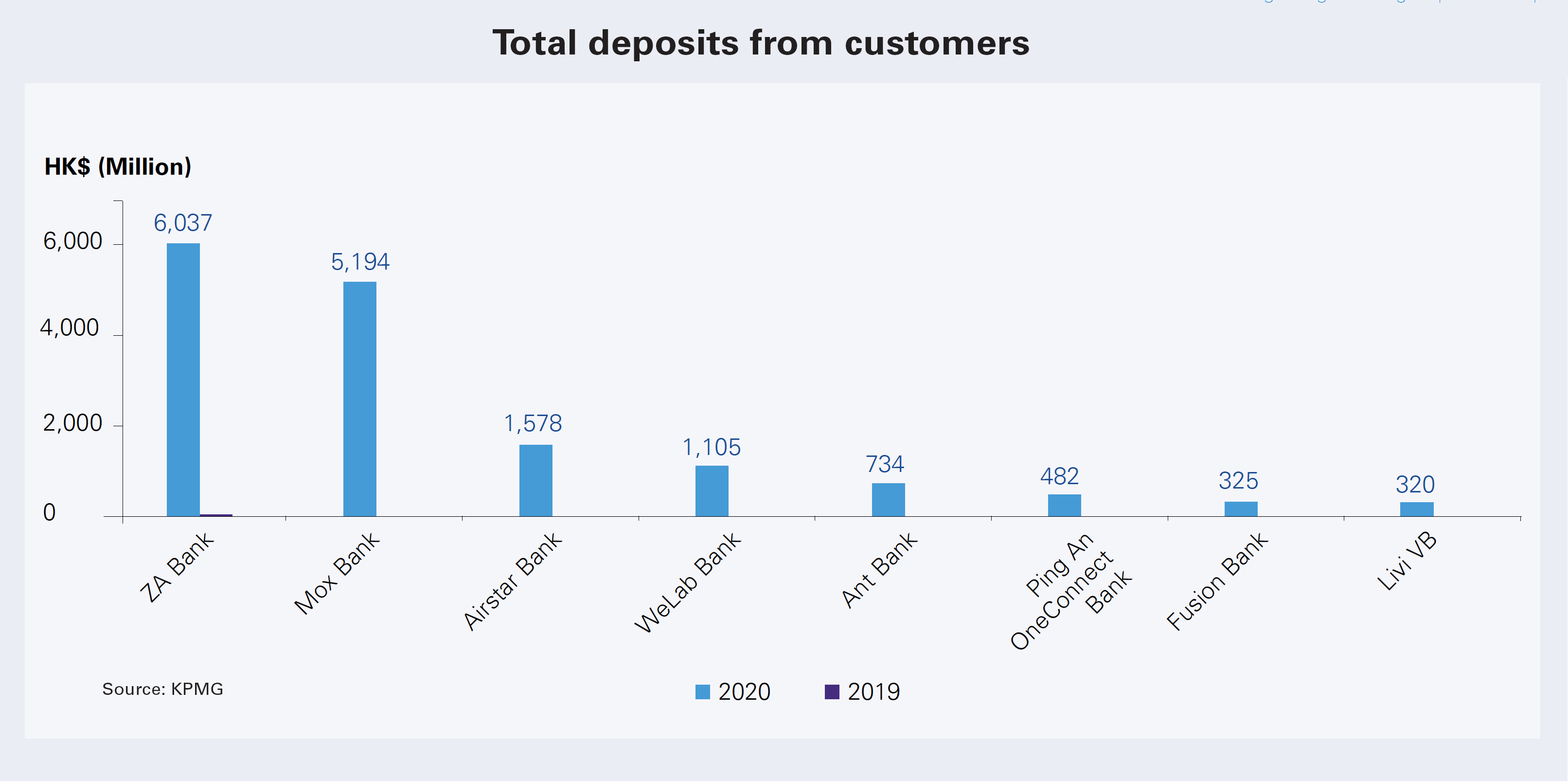

As of December 2020, their combined deposits reached HK$15.8 billion ( US$2 billion ), or 0.11% of total deposits across the entire banking sector. ZA Bank and Mox Bank had the largest share of deposits among all virtual banks at 38% and 33%, respectively.

In terms of loans, four of the virtual banks had advances to customers as of December 2020, although the amounts for Mox Bank and ZA Bank were negligible. Airstar Bank recorded a sizeable HK$557 million of loans to customers, while Ping An OneConnect Bank had about HK$70 million.

The virtual banks are expected to focus on offering more loans to their clients to boost revenue through interest income. In April Mox Bank became the first virtual bank in Hong Kong to launch its own credit card services through its all-in-one Mox Card, while Airstar Bank launched a pilot corporate banking service offering in May.

“In a fiercely competitive market like Hong Kong, it is essential for virtual banks to continue to expand their products and services to stand out from their peers – both traditional banks and other virtual banks – and gain a critical mass of customers and deposits. This should also include an increased focus on attracting not just retail clients, but also [small and medium-scale enterprises] to expand their customer base,” says Steve Cheung, partner, financial services, KPMG China.

Covid-19 has accelerated the adoption of technological innovations across the banking sector as a growing number of customers are embracing digital platforms and services.

“This can be viewed as both an opportunity and a challenge for virtual banks,” the report notes. “On the one hand, the growing awareness of digital platforms and services presents an opportunity for virtual banks – which have built their digital infrastructure from scratch – to offer bespoke products and an improved user experience to attract more customers.

“On the other hand, traditional banks in Hong Kong have been preparing for the launch of virtual banks for a few years, and the pandemic has also acted as a catalyst for these banks to accelerate their digital transformation initiatives, narrowing the digital gap between traditional and virtual banks.”

As such, virtual banks need to explore areas where they can make a difference, including providing competitive interest rates on customer deposits and introducing new products and services such as credit cards, loans and eventually wealth management services.

They can also leverage their partnerships with their key owners and stakeholders to provide value-added benefits and promotion schemes such as shopping discounts and other lifestyle benefits, the report says.